Inventory Growth and Market Balance

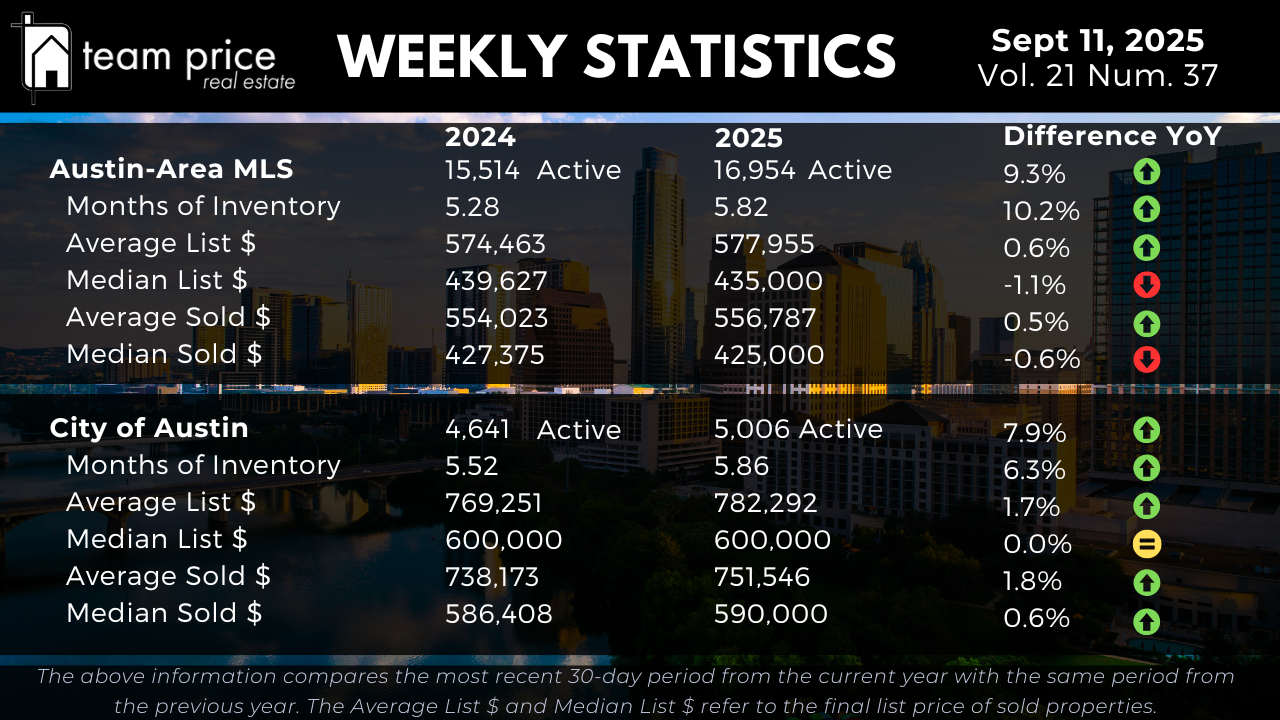

Active residential listings across the Austin-Area MLS climbed to 16,954 in September 2025, a 9.3 percent increase from 15,514 one year ago. Months of Inventory expanded from 5.28 to 5.82, marking a 10.2 percent rise and confirming that supply is building faster than demand. Within the City of Austin, the increase was slightly smaller but still notable. Active listings rose 7.9 percent year over year, moving from 4,641 to 5,006, while Months of Inventory increased from 5.52 to 5.86, a 6.3 percent gain. Together, these figures highlight a market where buyers have more choice, sellers face more competition, and absorption is slower than last year.

Pricing Stability Across the MLS

Price trends across the Austin-Area MLS show little movement, underscoring a market in search of stability. The average list price rose just 0.6 percent year over year, from $574,463 to $577,955, while the median list price slipped 1.1 percent to $435,000. Closed sales showed a similar pattern, with the average sold price up only 0.5 percent to $556,787, while the median sold price dipped 0.6 percent to $425,000. These figures confirm that while inventory is growing, buyers and sellers are finding common ground at price levels that are largely flat compared to a year ago.

Pricing Trends in the City of Austin

Inside the City of Austin, prices showed slightly more resilience than the regional market. The average list price increased 1.7 percent to $782,292, while the median list price held steady at $600,000. Closed sales reflected a modest upward trend, with the average sold price advancing 1.8 percent to $751,546 and the median sold price improving 0.6 percent to $590,000. While growth remains minimal, these results suggest that demand in Austin’s urban core is supporting stronger price stability compared to the broader metro.

Negotiation and Buyer Leverage

Negotiation remains a consistent feature of the Austin housing market. So far this month, 69.26 percent of closed sales have transacted below list price, up from 65.95 percent last month. The share of homes selling at list price dropped to 18.33 percent, while 12.41 percent of homes closed above asking, nearly unchanged from August but down from 13.24 percent in July 2024. The average sold-to-list price ratio now stands at 96.81 percent, underscoring that most buyers are still negotiating discounts relative to asking prices.

Regional and ZIP Code Variations

Conditions continue to vary across Central Texas. Of the 30 tracked cities, 14 (47 percent) posted month-over-month price increases, while 16 (53 percent) recorded declines. On a year-over-year basis, 12 cities (40 percent) saw gains and 18 (60 percent) saw losses. None of the 30 tracked cities are above their 12-month peak levels.

At the ZIP code level, 27 out of 75 tracked areas (36 percent) reported month-over-month increases, while 45 (60 percent) saw declines. On a year-over-year basis, 24 ZIP codes (32 percent) posted gains, while 51 (68 percent) recorded losses. Only one ZIP code in the region has exceeded its 12-month peak, leaving 74 still below. These figures show that recovery is inconsistent and highly localized, with certain areas stabilizing faster than others.

Prices Relative to Peak Levels

Both the Austin-Area MLS and the City of Austin remain well below their peak valuations from 2022 and 2023. Across the MLS, the average list price is down 11.8 percent from its March 2023 high, while the median list price has fallen 12.7 percent from May 2022. The average sold price is 17.7 percent below May 2022 levels, and the median sold price is down 22.9 percent. On a price-per-square-foot basis, values remain 22 to 24 percent lower than their peak.

In the City of Austin, declines are also evident. The average sold price is 14.6 percent below its May 2022 peak, and the median sold price is down 18.0 percent. Price-per-square-foot metrics in Austin are off by 22 to 26 percent compared to their highs. Even as list prices in the city show some stability, sold values remain meaningfully lower than peak conditions.

Market Outlook

The Austin housing market in mid-September 2025 reflects a period of balance rather than extremes. Inventory continues to expand, absorption has slowed, and buyers are negotiating successfully. Prices remain stable year over year, with the City of Austin showing slightly more strength than the regional MLS, but both remain well below their peak valuations. For buyers, this environment offers more choices and opportunities to secure discounts. For sellers, success hinges on accurate pricing and realistic expectations. For investors, the takeaway is clear: the market has shifted from the volatility of the past into a steadier phase, where long-term positioning and careful deal analysis are the keys to success.